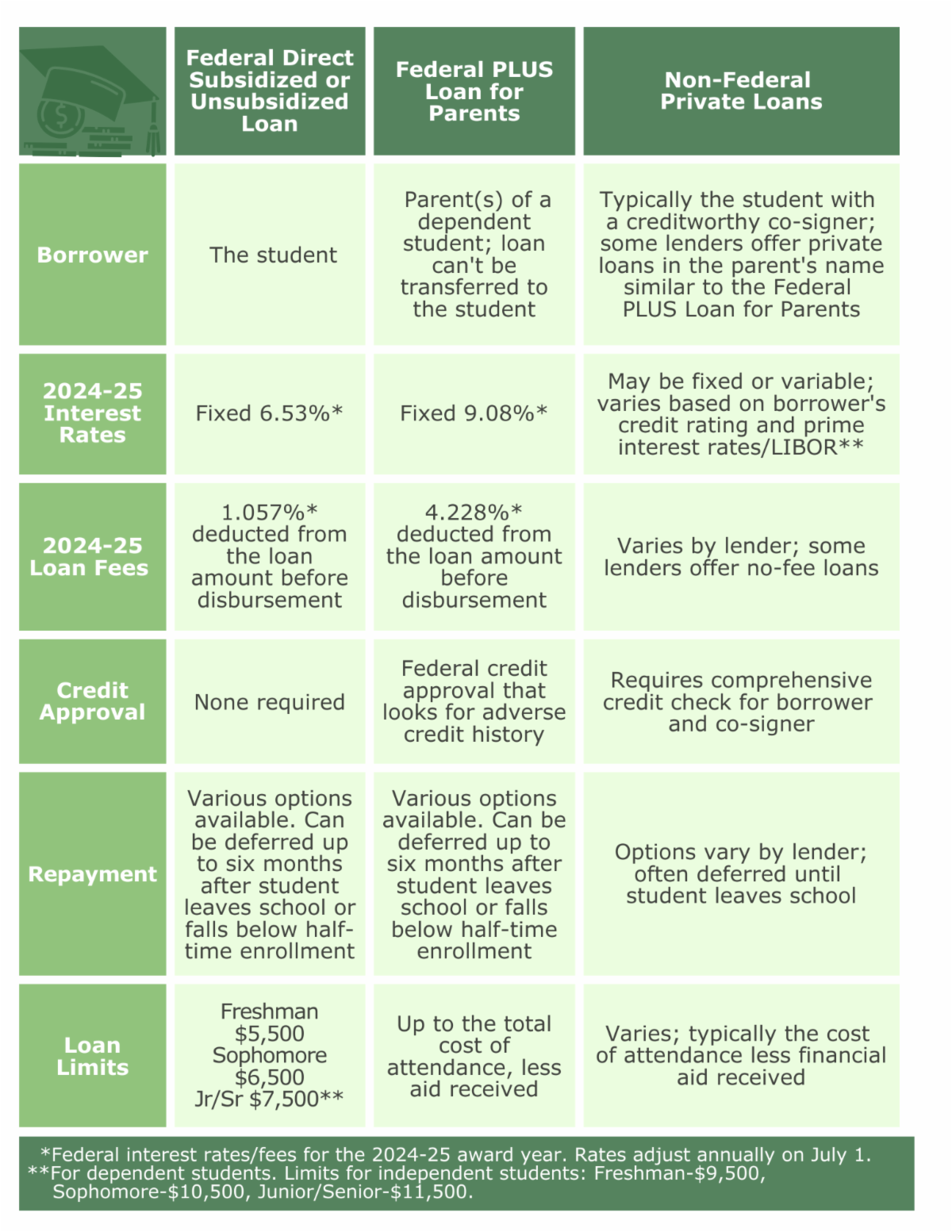

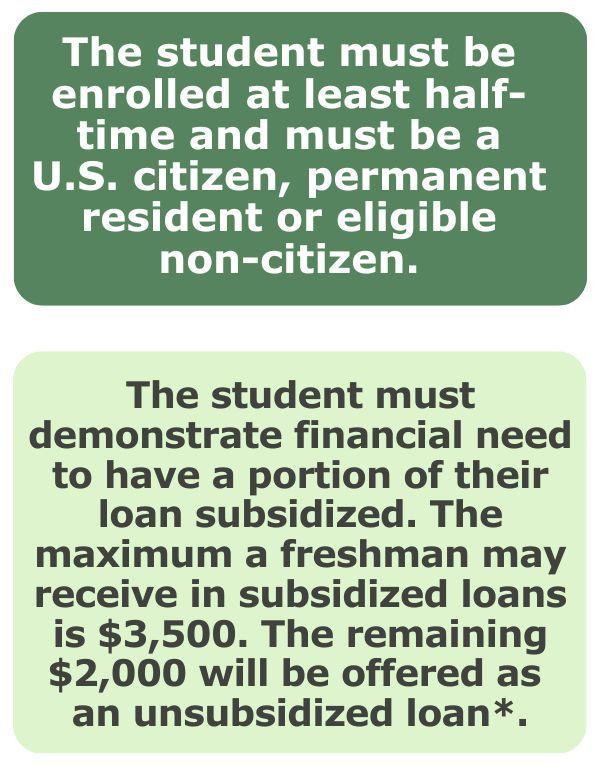

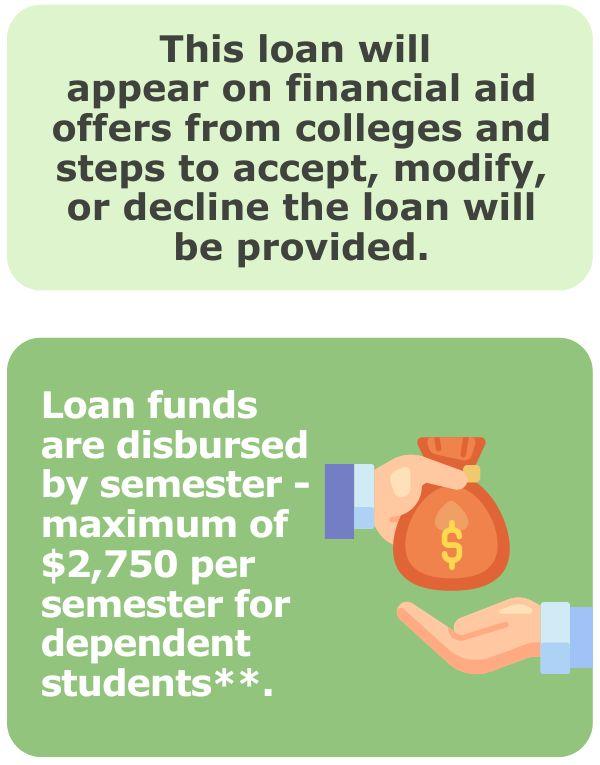

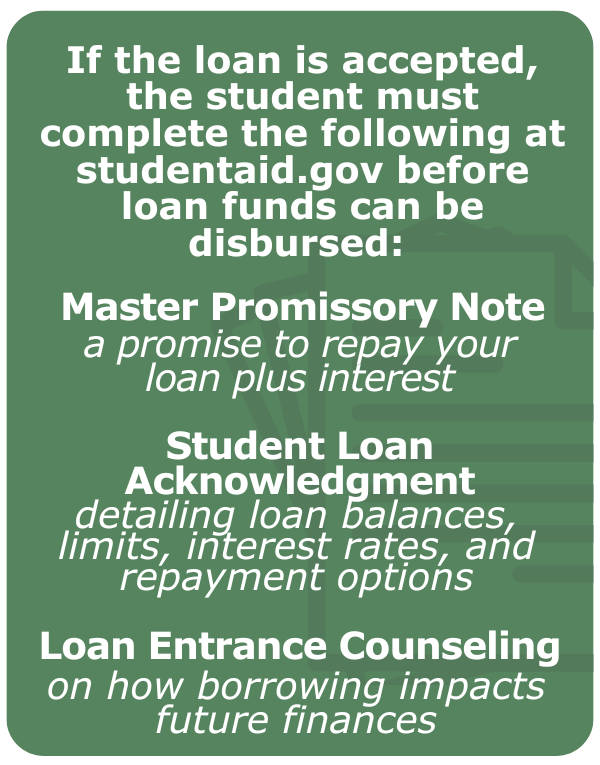

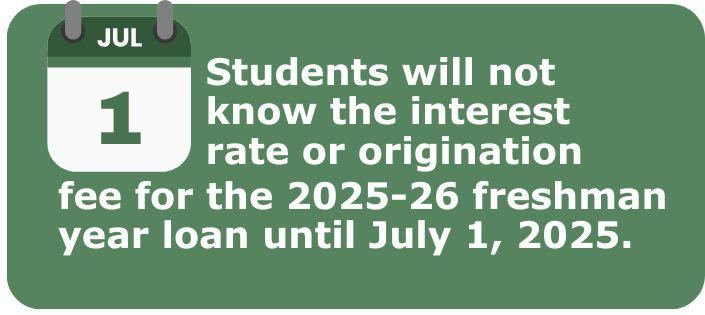

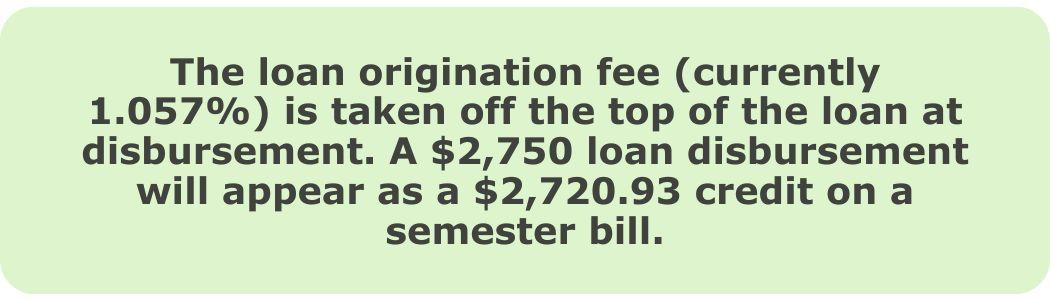

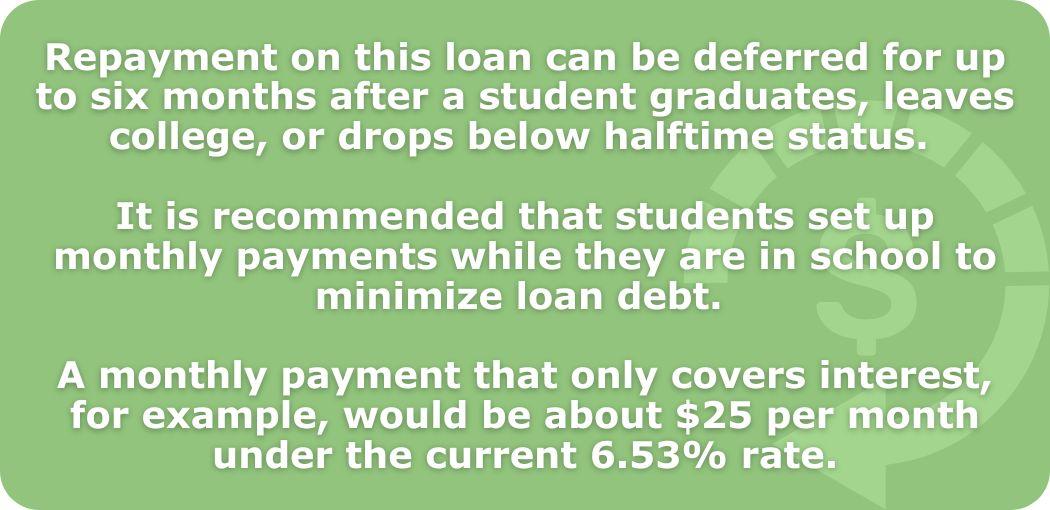

The Federal Direct Student Loan is typically the student's best option for borrowing entirely in the student's name without a co-signer based on its ease of access, low fixed interest rate, and repayment options. Therefore, it is usually in the student's best interest to maximize their federal student loan amount ($5,500 freshman year for dependent students, $9,500 for independent students) before considering alternative loan options to pay the gap. Here are some things to know about the Federal Direct Student Loan: |